Are 401k Losses Tax-Deductible?

- A 401(k) plan allows employees to invest part of their salary tax-free, and also allows them to borrow money from the plan.

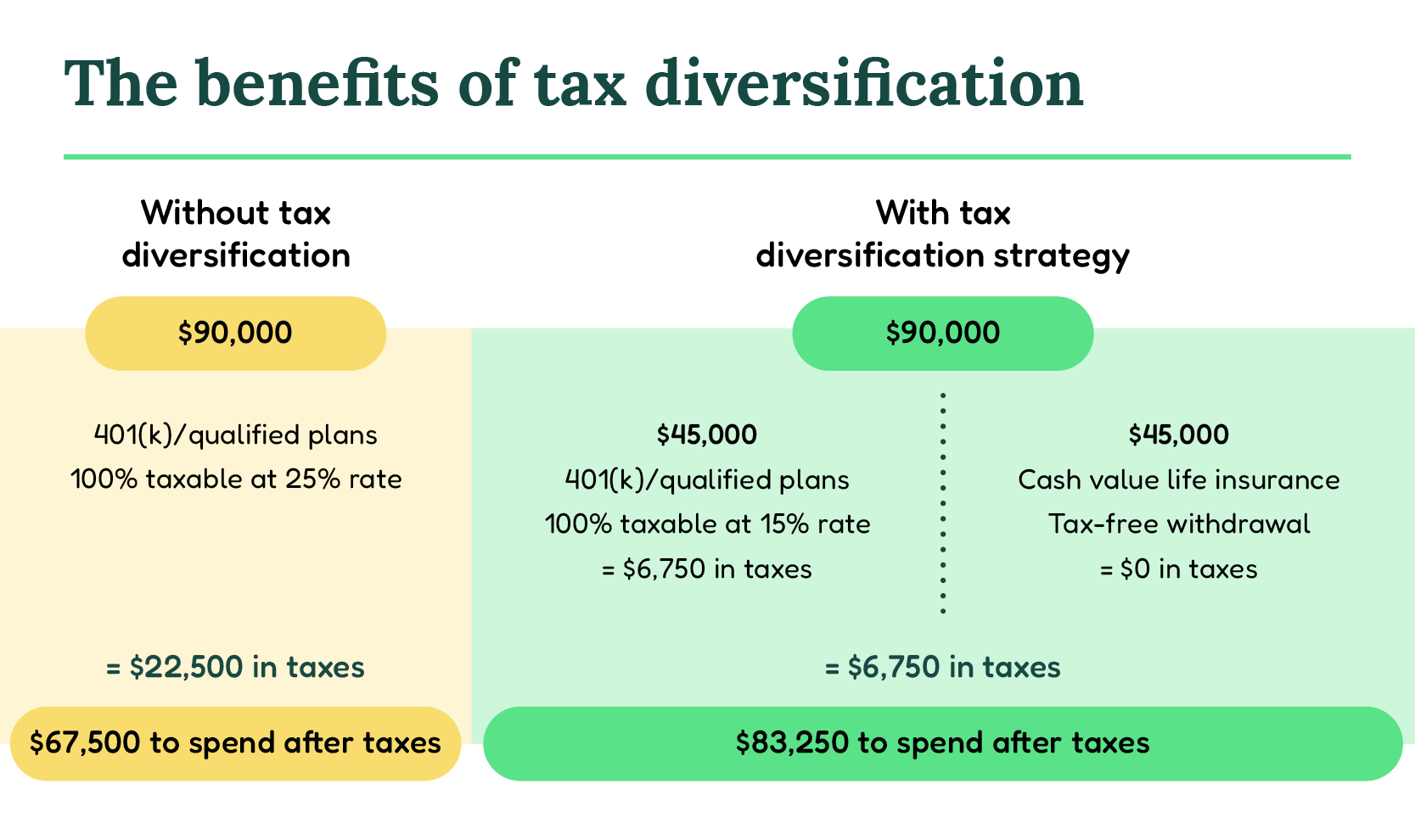

- A 401(k) plan allows individuals to invest money for retirement. 401(k) account withdrawals are taxed as regular income, while Roth IRA withdrawals are taxed as long-term capital gains.

The losses incurred in a 401(k) plan are not tax-deductible. However, money invested in a 401(k) account can be withdrawn tax-free. However, the tax implications will depend on how long you have held the particular funds in the 401(k) account.

401k Losses and the Tax Code

Under the tax code, taxpayers are allowed to deduct their 401k contributions to the extent of their modified adjusted gross income (MAGI).

MAGI is defined as adjusted gross income, plus any tax-exempt interest, plus any taxable interest, plus 50% of modified adjusted gross income (MAGI) from Schedule A deduction, plus 50% of self-employment tax, plus 50% of undistributed net investment income.

Since 401k contributions are made with pretax dollars, they do not reduce the taxable earnings of the taxpayer. Instead, the earnings are tax-free until withdrawal.

Tax-Deferred 401k Plans

A 401k plan allows investors to save for retirement on tax-deferred basis. However, tax-deferred accounts do not preclude you from paying taxes.

If you withdraw money from your 401k plan before age 59 1/2, you are subject to an early withdrawal tax.

401k Plan With Roth

There are certain instances when losses in an individual retirement account (IRA) are fully or partially deductible. The Internal Revenue Service (IRS) has a list of circumstances under which a deductible loss is allowed including:

A casualty loss is incurred as a result of a natural disaster, such as a flood, fire, or hurricane.

The loss results from theft or embezzlement.

The loss occurs as a result of a legal dispute.

The loss results from casualty to property outside of the U.S.

The loss results from casualty to the primary residence.

A taxpayer who incurs a casualty loss from theft, embezzlement, or a legal dispute is not allowed to deduct the entire loss. Instead, the IRS allows the taxpayer to deduct the amount of loss that would result from a casualty.

For example, if a taxpayer purchases an investment that loses 20% in value, 20% of the loss would not be deductible. However, if the investment lost 40% in value, the entire loss of $10,000 would be deductible.

401k Plan With Employer Match

If you contribute to a 401k plan with an employer match, your contributions plus the match are tax-deductible (though this deduction phases out based on your income). So, if you contribute $5,000 and your employer matches $5,000, then it's $10,000 of compensation that is tax-deductible (though this deduction phases out based on your income).

401k Plan Without Employer Match

If you're enrolled in a 401k plan without an employer match, then only your contributions - up to $19,000 in 2021 - are tax-deductible.

Roth IRA

While contributions to a Roth IRA are generally not tax-deductible, earnings are tax-free in retirement. One caveat: Roth IRAs, unlike 401k plans, do not require that your income be under a certain threshold ($120,000 in 2021).

401k Plan With Profit Sharing

Losses incurred on investments held in a profit-sharing 401k plan are deductible up to $3,000 annually. Losses in excess of this amount can be carried forward and deducted in future years.

401k Plan With Nonprofit Employer

Losses incurred on investments held in a plan sponsored by a nonprofit organization are deductible up to $3,000 annually. Losses in excess of this amount can be carried forward and deducted in future years.

401k Plan With Profit-Sharing Employer

Losses incurred on investments held in a profit-sharing 401k plan are deductible up to $3,000 annually. Losses in excess of this amount can be carried forward and deducted in future years.

401k Plan With Non Profit-Sharing Employer

Losses incurred on investments held in a plan sponsored by a nonprofit organization are deductible up to $3,000 annually. Losses in excess of this amount can be carried forward and deducted in future years.

401k Plan With Non Profit-Sharing Employer That Has More Than 100 Participants

Losses incurred on investments held in a plan sponsored by a nonprofit organization are deductible up to $3,000 annually. Losses in excess of this amount can be carried forward and deducted in future years.

401k Plan With Defined Contribution

The tax treatment of 401k plan distributions depends on the plan design.

A 401k plan with defined contribution (DC) is one of the more common plan designs. In this type of 401k plan, the employee decides how much to contribute. The employer may also contribute to an employee's account, though this is less common.

Each employee's contributions and any employer contributions are placed into a retirement account, such as a brokerage account. When the employee retires, he or she takes distributions from the account.

Under DC plan rules, withdrawals are taxable as ordinary income. However, if the employee is under age 59 1⁄2, the distribution is included in the employee's income for that year and is subject to a 10% penalty.

401k Plan With Defined Benefit

The rules for 401k plans with a defined benefit are slightly different than the rules for those without a defined benefit.

The employer deducts the contribution and the employee's account value grows tax-free. The employer and employee contributions are tax-deductible.

The employee pays taxes on a distribution that occurs when the employee reaches age 59 1/2 or turns 70 1/2. Distributions before age 59 1/2 are penalized by 10% in income taxes and a 10% IRS penalty. Distributions before age 59 1/2 and before age 70 1/2 that are due to disability are also penalized by 50% in income taxes and a 50% IRS penalty.

Distributions before age 59 1/2 and before age 70 1/2 that are due to death are penalized by 25% in income taxes and a 25% IRS penalty.

401k Plan With Defined Contribution

Although a 401k plan with a defined benefit is tax deductible for the employer, contributions are not tax-deductible for the employee.

Contributions to a 401k plan are tax-deductible for the employer.

The employee pays taxes on distributions that occur when the employee reaches age 59 1/2 or turns 70 1/2. Distributions before age 59 1/2 are penalized by 10% in income taxes and a 10% IRS penalty. Distributions before age 59 1/2 and before age 70 1/2 that are due to disability are also penalized by 50% in income taxes and a 50% IRS penalty.

Distributions before age 59 1/2 and before age 70 1/2 that are due to death are penalized by 25% in income taxes and a 25% IRS penalty.

401k Plan With Salary Deferral

If you actively participate in a 401k plan offered by an employer with salary deferral, your 401k plan contributions and earnings are not taxable until withdrawn.

A 401k plan with a salary deferral feature offers the opportunity to save for retirement on a tax-deferred basis. However, when participants withdraw from their 401k plan, the withdrawal amount is taxable as ordinary income, and they are subject to ordinary income taxes.

401k Plan With Defined Benefit and Fund Options

In plans with defined benefit (DB) options, which are now allowed in 401k plans, the losses incurred by the plan participant are tax-deductable.

In the event of DB plan termination, the plan sponsor may distribute the fair market value (FMV) of the plan participant's account. In this case, any losses realized by the plan participant are taxable.

401k Plan With Self-Directed Options

In self-directed 401k plans, the plan participant may invest the 401k account into a variety of investments. Therefore, the plan participant may incur losses due to unfavorable market conditions. However, the losses incurred by the plan participant in a self-directed 401k plan are not tax deductible.

401k Plan With Defined Benefit and Profit Sharing

A defined benefit plan is a type of retirement plan that provides a set monthly benefit upon retirement. The benefit is based on an employee's salary and the number of years worked, and is paid out even if the employee chooses to leave the plan before retirement.

A profit sharing plan is a type of retirement plan that allows employees to pick investments and share in the profits. Profit sharing plans are discretionary, and the contributions made are discretionary as well. Unlike 401k plans, profit sharing plans are not tax-deferred.

401k Plan With Defined Benefit and Salary Deferral

Yes.

If you contribute to a 401k plan, and your employer's contributions to your plan are tax-deductible, then your contributions - as pre-taxed income - are also tax-deductible.

In 2018, the maximum amount an individual can contribute to a 401k plan - pre-taxed - is $18,500. For those who make less than $18,500 in annual compensation, an additional $6,000 can be contributed as a "catch-up" contribution.

401k Plan With Defined Benefit, Profit Sharing, and Salary Deferral

If you become unemployed, retire, or leave your employer, or if your company closes, your 401k plan balance will be subject to taxes. However, your 401k plan balance is subject to taxes only when it is distributed. You can defer income taxes on 401k earnings until withdrawal.

When you leave an employer, your plan balance will be subject to taxes. You can avoid taxes by rolling the money over into an IRA or rolling it into your current employer's retirement plan.

401k Plan With Defined Benefit, Profit Sharing, and Employer Match

Losses incurred in a defined benefit retirement plan are tax-deductible if the plan's acquisition costs are deductible. However, gains in a defined benefit plan are not tax-deductible.

As with defined contribution plans, losses incurred in a defined contribution plan are tax-deductible unless the contributions are after-tax.

401k Plan With Defined Contribution Only

Losses incurred in a defined contribution plan are not tax-deductible.

401k Plan With Only Employer Match

Losses incurred in a plan with an employer match are not tax-deductible.

401k Plan With Both Defined Benefit and Employer Match

Losses incurred in a plan with both defined benefits and an employer match are not tax-deductible.

401k Plan With Defined Benefit, Profit Sharing, Employer Match, and Salary Deferral

If you contribute to a 401k plan, your total contribution for the year is included in the total income on your IRS tax return, with taxes due on the total dollar amount contributed.

If you withdraw money from your employer-sponsored 401k plan, the amount withdrawn is included in the income on your return, but any earnings on the money inside the account are taxed at only the capital gains rate.

401k Plan With Defined Contribution Only

If you contribute to a 401k plan, your contribution is not included in the total income on your IRS tax return. Your employer matches are not included.

If you receive a distribution from your 401k plan, the amount withdrawn is included in the income on your return, but any earnings on the money inside the account are taxed at the capital gains rate.

Yes, if you invest in a company's stock and do not sell it until after it has gone bust, your losses are tax-deductible.

The IRS allows taxpayers to reduce their taxable income by the amount of their losses, up to certain limits. In 2021, you can deduct up to $3,000 per year of net losses from investments held in your IRA, 401k, or 403b plans.

401k Plan With Defined Benefit, Profit Sharing, Employer Match, and Defined Contribution

A 401k plan with defined benefit, profit sharing, employer match, and defined contribution (DB/RS/E/C) allows for tax-deferred growth of assets. This includes employer contributions and any earnings that may result from those contributions. However, any withdrawals that are made from the 401k plan are taxable.

Gold IRA: Should You Open One To Save For Retirement?

401k Plan With

No Rollover

A 401k plan with no rollover option doesn't contain a direct way to move funds into another account. Thus, the only way for a 401k plan participant to withdraw funds from their account would be to withdraw the funds in cash.

However, any funds withdrawn from the 401k plan are taxable as ordinary income. A 401k plan sponsor may allow a participant to rollover funds from one qualified account to another, such as from an IRA to a 401k plan.