The Cost of Perspective Software for Your IRA Plan

- Software programs can be used to manage your individual retirement account (IRA).

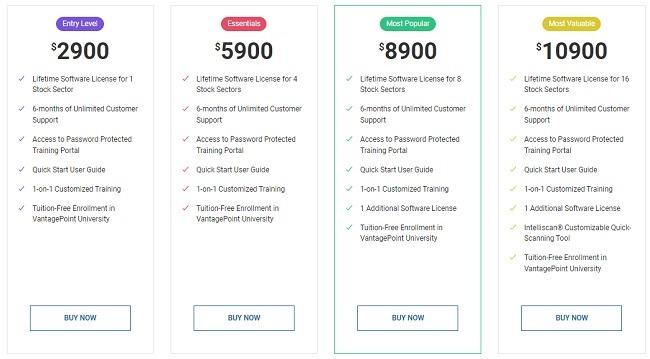

- These software packages include account aggregation, trading, tax loss harvesting, rebalancing, and tax reporting.

- Fees for these services vary, and the software can be purchased and downloaded from the company website, or it can be hosted on cloud servers.

- Investing in the financial markets can be time consuming, confusing and expensive.

Investing in the financial markets can be time consuming, confusing and expensive. Many professional investors and traders employ software programs to help them get a better handle on their investments. This article discusses the cost and availability of software that can be used to help you manage your individual retirement account (IRA).

A Primer on Software for IRAs

The 401(k) plan is one of the most widely used employer-sponsored retirement plans available. As such, many traditional IRA plans allow a rollover from a 401(k) plan. The Internal Revenue Service (IRS) offers the following guidelines for a rollover from a 401(k) plan:

The IRA trustee must be the plan sponsor.

The trustee must be a financial institution.

The trustee must be insured by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA).

The IRA trustee must have reasonable written policies and procedures for recordkeeping, delivery of checks and tax withholdings, and for the administration of distributions.

How Does the IRA Software Work?

Most self-directed IRA providers use third-party software, like PlanPlus, to help facilitate investments. Using such software, you can open various retirement accounts, including IRAs, for your clients. The software also allows you to track your client's investments. The software allows you to generate tax forms (1099-DIV, 1099-R, etc.) for your clients and report investment gains or losses for them. The software automates the entire process of signing up a new client, opening a new account, and facilitating investments.

The software also handles all the recordkeeping functions. The software tracks your clients' investments, generates tax forms, and keeps track of client-investor meetings. It also has built-in compliance monitoring.

Advantages of Software for IRAs

Software for IRAs allows plan administrators to more easily track assets, beneficiaries, and distributions.

IRA software can help plan administrators comply with the Employee Retirement Income Security Act (ERISA).

This software can help plan administrators demonstrate their adherence to ERISA rules and requirements.

Disadvantages of Software for IRAs

This software requires users to be proficient in computers, the internet, and software.

This software can be expensive, and is not typically necessary when using other tracking tools.

Disadvantages of Software for IRAs

Many of the disadvantages of investing in precious metals are not present when using software for self-directed IRAs to buy physical precious metals. These include:

Storage of precious metals: Some physical precious metals brokers store metals in facilities that do not have insurance against natural disasters. You would be liable for the value of the metals in the event of a disaster.

Shipping of precious metals: Some brokers do not ship precious metals.

Insurance of precious metals: Some brokers do not have insurance for precious metals.

Restrictions on buying: Some brokers limit the amount of precious metals you can buy.

Choosing a Software Vendor for Your IRAs

There are three major types of software to choose from:

1. Self-Directed IRA Custodian Software

2. Third-Party IRA Custodian Software

3. Self-Directed IRA Software

The Self-Directed IRA Custodian Software provides custodian-specific features, but the software may be less flexible, especially for noncustodial IRAs. The Self-Directed IRA Software is a good choice for IRAs without custodian involvement, such as for traditional IRAs.